استرجاع مجاني وسهل

استرجاع مجاني وسهل أفضل العروض

أفضل العروض

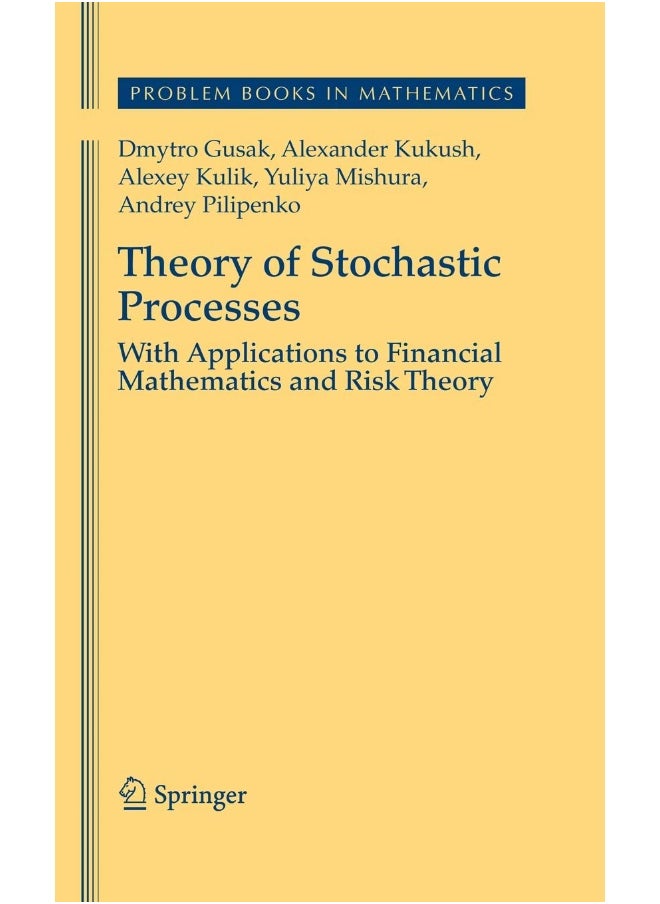

| الناشر | Springer; 2010th edition |

| رقم الكتاب المعياري الدولي 13 | 9781461425069 |

| رقم الكتاب المعياري الدولي 10 | 1461425069 |

| الكاتب | Dmytro Gusak |

| تنسيق الكتاب | Paperback |

| اللغة | English |

| وصف الكتاب | Definition of stochastic process. Cylinder #x03C3;-algebra, finite-dimensional distributions, the Kolmogorov theorem.- Characteristics of a stochastic process. Mean and covariance functions. Characteristic functions.- Trajectories. Modifications. Filtrations.- Continuity. Differentiability. Integrability.- Stochastic processes with independent increments. Wiener and Poisson processes. Poisson point measures.- Gaussian processes.- Martingales and related processes in discrete and continuous time. Stopping times.- Stationary discrete- and continuous-time processes. Stochastic integral over measure with orthogonal values.- Prediction and interpolation.- Markov chains: Discrete and continuous time.- Renewal theory. Queueing theory.- Markov and diffusion processes.- It#x00F4; stochastic integral. It#x00F4; formula. Tanaka formula.- Stochastic differential equations.- Optimal stopping of random sequences and processes.- Measures in a functional spaces. Weak convergence, probability metrics. Functional limit theorems.- Statistics of stochastic processes.- Stochastic processes in financial mathematics (discrete time).- Stochastic processes in financial mathematics (continuous time).- Basic functionals of the risk theory. |

| تاريخ النشر | 3 May 2012 |

| عدد الصفحات | 388 pages |

![/fashion-men/jack_jones/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-04.png)

![/fashion-men/seventy_five/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-01.png)

![/fashion-men/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-02.png)

![/fashion-women/mango/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-05.png)

![/fashion-women/guess/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-09.png)

![/fashion-women/ella/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-01.png)

![/fashion-women/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-02.png)

![/fashion/view-all-kids-clothing/nike/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-01.png)

![/fashion/view-all-kids-clothing/disney/disney_minnie_mouse/disney_frozen/disney_princess/disney_mickey_mouse/disney_baby/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-03.png)

![/fashion/view-all-kids-clothing/new_balance/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-11.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/chloris/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-04.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/roland/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-05.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/donner/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-06.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/korg/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-07.png)