Free & Easy Returns

Free & Easy Returns Best Deals

Best Deals

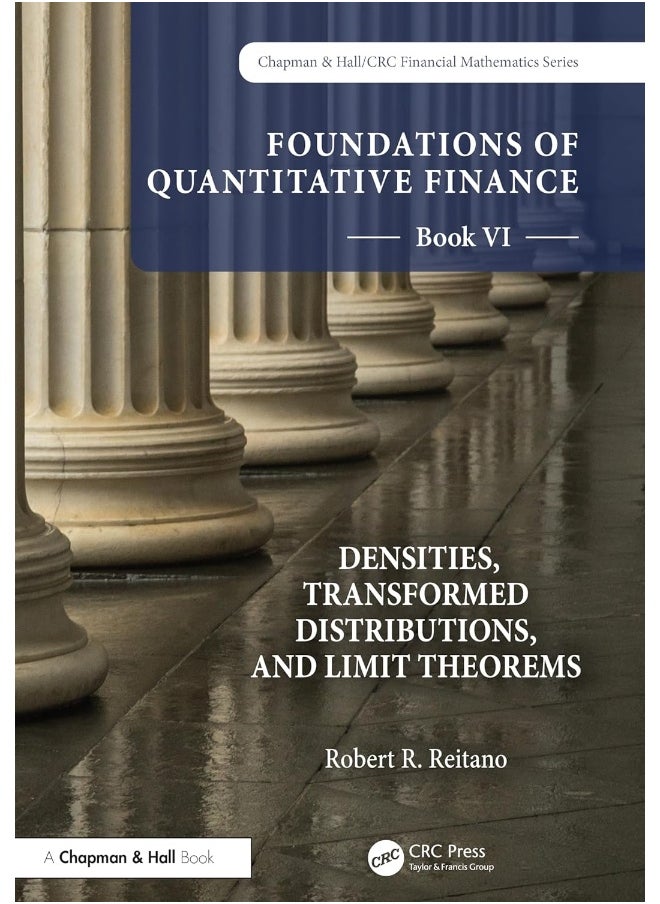

| Publisher | Chapman and Hall/CRC |

| ISBN 13 | 9781032229492 |

| ISBN 10 | 1032229497 |

| Author | Robert R. Reitano |

| Book Format | Paperback |

| Language | English |

| Book Description | Every finance professional wants and needs a competitive edge. A firm foundation in advanced mathematics can translate into dramatic advantages to professionals willing to obtain it. Many are not―and that is the competitive edge these books offer the astute reader.Published under the collective title of Foundations of Quantitative Finance, this set of ten books develops the advanced topics in mathematics that finance professionals need to advance their careers. These books expand the theory most do not learn in graduate finance programs, or in most financial mathematics undergraduate and graduate courses.As an investment executive and authoritative instructor, Robert R. Reitano presents the mathematical theories he encountered and used in nearly three decades in the financial services industry and two decades in academia where he taught in highly respected graduate programs.Readers should be quantitatively literate and familiar with the developments in the earlier books in the set. While the set offers a continuous progression through these topics, each title can be studied independently.FeaturesExtensively referenced to materials from earlier booksPresents the theory needed to support advanced applicationsSupplements previous training in mathematics, with more detailed developmentsBuilt from the author's five decades of experience in industry, research, and teachingPublished and forthcoming titles in the Robert R. Reitano Quantitative Finance Series:Book I: Measure Spaces and Measurable FunctionsBook II: Probability Spaces and Random VariablesBook III: The Integrals of Riemann, Lebesgue and (Riemann-)StieltjesBook IV: Distribution Functions and ExpectationsBook V: General Measure and Integration TheoryBook VI: Densities, Transformed Distributions, and Limit TheoremsBook VII: Brownian Motion and Other Stochastic ProcessesBook VIII: Itô Integration and Stochastic Calculus 1Book IX: Stochastic Calculus 2 and Stochastic Differential EquationsBook X: Classical Models and Applications in Finance |

| About the Author | Robert R. Reitano is Professor of the Practice of Finance at the Brandeis International Business School where he specializes in risk management and quantitative finance, and where he previously served as MSF Program Director, and Senior Academic Director. He has a Ph.D. in Mathematics from MIT, is a Fellow of the Society of Actuaries, and a Chartered Enterprise Risk Analyst. He has taught as Visiting Professor at Wuhan University of Technology School of Economics, Reykjavik University School of Business, and as Adjunct Professor in Boston University’s Masters Degree program in Mathematical Finance. Dr. Reitano consults in investment strategy and asset/liability risk management and previously had a 29-year career at John Hancock/Manulife in investment strategy and asset/liability management, advancing to Executive Vice President & Chief Investment Strategist. His research papers have appeared in a number of journals and have won an Annual Prize of the Society of Actuaries and two F.M. |

| Publication Date | 12 November 2024 |

| Number of Pages | 386 pages |

![/fashion-men/jack_jones/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-04.png)

![/fashion-men/seventy_five/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-01.png)

![/fashion-men/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-02.png)

![/fashion-women/mango/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-05.png)

![/fashion-women/guess/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-09.png)

![/fashion-women/ella/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-01.png)

![/fashion-women/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-02.png)

![/fashion/view-all-kids-clothing/nike/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-01.png)

![/fashion/view-all-kids-clothing/disney/disney_minnie_mouse/disney_frozen/disney_princess/disney_mickey_mouse/disney_baby/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-03.png)

![/fashion/view-all-kids-clothing/new_balance/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-11.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/chloris/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-04.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/roland/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-05.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/donner/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-06.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/korg/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-07.png)